Will homeowners be better off in retirement?

Roughly two thirds of people expect to own their home in retirement. Provided that they are largely mortgage free by the time they retire, these people will not only save substantial amounts on rent, but they’ll also have the option to build up equity which they then can potentially access through equity release.

Typically a retired homeowner might access around a third of their equity, and the average value that is accessible will vary across the country, mirroring house prices. For most regions of the UK, typical equity release could provide an additional £60,000 to fund retirement. In the South East this doubles to over £120,000, and in London it’s over £170,000.

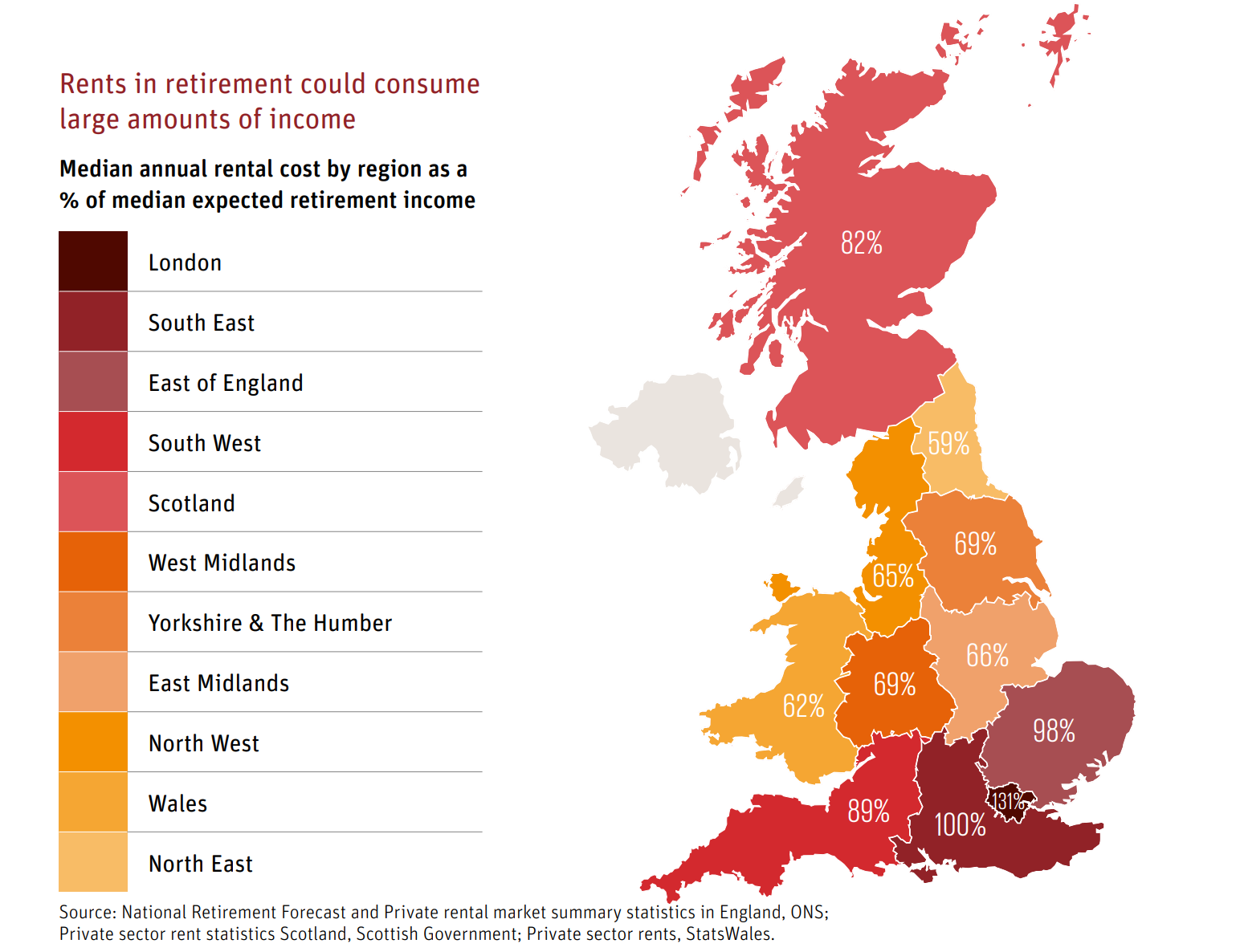

Access to housing is crucial in order to enhance retirement outcomes. Improving housing affordability is central to this, and means we need to ramp up house building. This would result in renting being more affordable, and fewer would need to rent in retirement if they could get on the housing ladder.

Retirement expectations vs reality – homeowners vs renters

Scottish Widows’ Retirement Report demonstrates more clearly than ever that while many are making good preparations for retirement, a substantial minority are being left behind. While addressing the high cost of living is rightly the government’s priority for the time being, as inflation goes down and conditions begin to stabilise, more needs to be done to address the long-term reforms and enhancements to automatic enrolment if savers are to enjoy a comfortable retirement income.

Automatic enrolment has undoubtedly been a game changer, with many savers in their 30s now likely to reach a comfortable retirement lifestyle, with auto enrolment playing no small part in establishing these strong saving behaviours.

The self-employed have also not benefited from automatic enrolment and as a result are much less likely to be saving into a pension. The forecast shows that while the self-employed do proportionately save more outside of a pension, this is not nearly enough to close the gap.

The report also shows the important role that a variety of assets have in retirement. Workplace Pensions and Personal Pensions are central, but so too is the state pension, wider savings that individuals accumulate or inherit and the equity that many build up in their homes. People need to be getting guidance, advice and support that brings all of these elements together to help them plan effectively for their retirement.

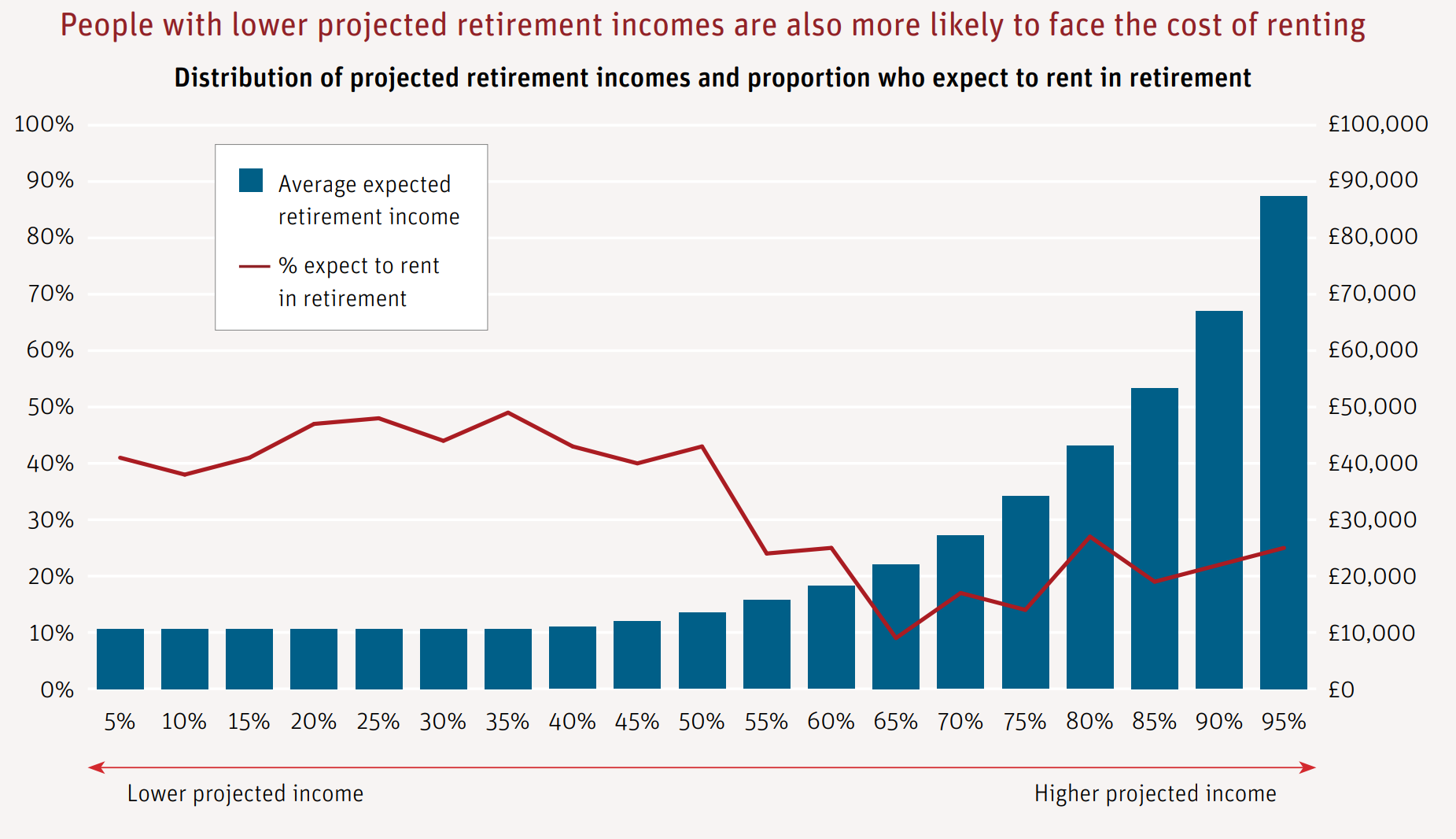

Our findings also highlight the disparities between those who are likely to rent in retirement and those who will own a home. Those on lower incomes are disincentivised from saving for retirement and are encouraged to rely on housing benefit, while those on middle incomes save too little to cover their rent and end up facing a much poorer retirement than they expect.