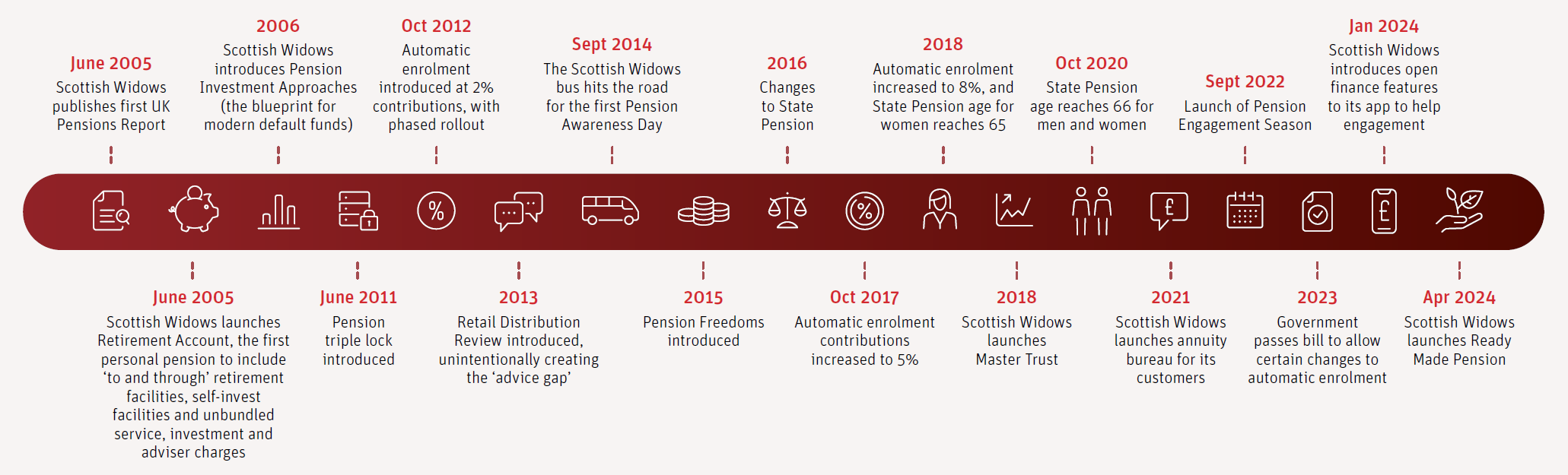

The introduction of automatic enrolment has been the biggest positive change in pensions. Since its introduction in 2012, more than 10 million extra savers have been brought into workplace pension saving for the first time. Opt-out rates have been lower than anyone predicted, and even during the pandemic when some people faced significant financial hardship, there was no discernible increase in opt-outs.

But while the policy helps a vast number of workers achieve a higher income in retirement, many will still be falling short of the savings they need to be making now if they are going to have a comfortable lifestyle when they get older.

To address this, we need contributions to rise from the current 8% to 12 % (with strong guidance that those who can afford to do so save 15%) of all earnings, for the full power of automatic enrolment to be realised.

Aside from automatic enrolment, the UK needs to continue progress in adapting its pension systems to the modern world. People change jobs more than they did in the past and there is more fluid movement between people choosing to work full time or part time, and employed or self-employed. The retirement system needs to adapt to fit the complexities of modern life. We are also living much longer and its not possible to save enough money during a working life of just 40 years to pay for a retirement which could last 30 years.

Part-time and self-employed workers are more likely to face worse retirement outcomes

There are over four million self-employed workers in the UK who are currently excluded from auto enrolment. 41% of part-time employees aren’t on track for even a minimum lifestyle in retirement (compared to 25% of full-time employees). This is driven by part-time workers earning less, but also because many of them don’t qualify for automatic enrolment as they fall below the threshold of earning £10k per year. Multi-jobbers could have total earnings of £24k across three jobs each paying £8k, with none of those employments triggering auto enrolment.

There’s also currently no equivalency of auto enrolment for self-employed workers, and as a result, 38% of self-employed workers aren’t on track for even a minimum lifestyle in retirement. This needs to be urgently addressed so that retirement provision becomes par for the course, no matter what type of work someone is in.

How do we improve retirement outcomes for self-employed and part-time workers?

To help improve retirement outcomes for those working part-time, we believe that the £10k earnings threshold at which workers are auto enrolled should be abolished. However, workers on those very low levels of earnings should be able to opt out of the employee contribution, whilst still benefiting from an employer contribution towards their retirement.

This is on the premise that no-one should be too poor to receive a contribution from their employer towards their retirement.

Women, the disabled, some ethnic groups and many within the LGBTQ+ community are also over-represented in these forms of employment, and these reforms would go a long way to addressing some of the polarisation that we see in projected outcomes across different cohorts of the population.